Interesting Banknotes Around the World

Let’s take a look at some of the world’s most interesting banknotes

Last week I looked at Canadian banknotes and how interesting they can be. But other nations’ money can provide some entertainment too!

Israel

Israeli lira from 1968 featured a portrait of Albert Einstein. You can still buy it on eBay for roughly $10 if you happen to be a big fan of his. Not many people know it, but Albert Einstein was offered Israeli presidency back in 1952 but turned it down.

Interesting Banknotes

Serbia

Serbian dinar also features a man of science - Nicola Tesla himself. The back side features a picture of electro-magnetic induction engine.

Interesting Banknotes

Turkey

Turkey went all math instead of physics. Their banknotes have a portrait of Cahit Arf - Turkish mathematician. While I consider myself fairly knowledgeable in math, I couldn’t even being to understand which part of mathematics he’s famous for.

Interesting Banknotes

Canada

Did you know that Canada used to have a 4-dollar banknote? They date back to early 1900, and were withdrawn from circulation shortly after.

Interesting Banknotes

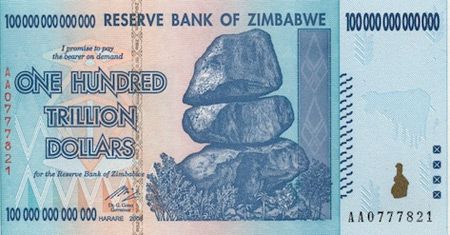

Zimbabwe

Zimbabwe went through a brutal cycle of hyperinflation - money was being printed with no regard to state of economy. More money flooded the market, and prices kept rising to no end. The banknotes issued risen in denomination. Below is a banknote for one hundred trillion dollars - probably just enough to fill up your car with gas!

Interesting Banknotes

Congo

Democratic Republic of Congo used to be known as Zaire. Joseph Mobutu ruled the country until he was overthrown in 1997. Instead of producing brand new money, new govt decided to punch holes in old money to get rid of his face - that resulted in producing banknotes with holes in them. I guess he wasn’t very popular, and everybody was sick of his face.

Interesting Banknotes

Canadian Banknotes are fascinating! - $50

Canadian banknotes can be truly fascinating!

Personally, I think Canadian banknotes are truly unique. Especially the latest series - so-called “polymer series”. Being basically plastic, they’re designed to be extra durable - and thus saving money on printing and replacing (God knows they’re printing enough money already). They also have a myriad of security features paper money didn’t have - holographic elements, transparent windows, raised characters, hidden numbers.

I especially like certain elements of Canadian pride shown on our money. Have you ever wondered who are the people pictured on our money? Even pictures on back sides are connected to Canadian history. Why are they shown there?

I had nothing to do this Sunday, so I’ve looked up some information on Canadian banknotes and imagery on them. So, next time you’re trying to make small talk with a good-looking cashier when grocery shopping, feel free to pass on this information.

Front Side - William Lyon Mackenzie King:

Canadian Banknotes

William Lyon Mackenzie King was a political figure in Canada from 1920’s and well into 1940’s. He served as a Prime Minster of Canada on multiple occasions, and some of his achievements can still be enjoyed today by everyday Canadians.

Notable achievements and interesting facts:

- William Lyon Mackenzie King was the longest serving Prime Minister of Canada - he ruled Canada for over 22 years .

- He wasn’t very popular with voters (despite being elected a number of times) and would probably never get elected if he was alive today, but he was a true diplomat and had a talent for striking alliances.

- Mackenzie King had five university degrees (his student loans must have been huge!)

- His government created Canadian Broadcasting Corporation (CBC) in 1936

- Trans-Canadian Airlines (now knows as Air Canada) was also created under his rule in 1937

- He transformed Bank of Canada into a crown corporation in 1938 (before that it used to be a private entity)

- William Lyon Mackenzie King is rated #1 (or the Greatest Prime Minister) by a survey of Canadian historians

Famous quote of William Lyon Mackenzie King (one of many):

“A true man does not only stand up for himself, he stands up for those that do not have the ability to”.

Back Side - CCGS Amundsen:

Canadian Banknotes

CCGS Amundsen is an Arctic icebreaker and research vessel operated by Canadian Coast Guard. Originally known as CCGS Sir John Franklin, this icebreaker was built in 1979 in North Vancouver. After serving for a number of years, it was decommissioned after it was deemed surplus (fancy term for “useless” or “not needed”).

In 2003, CCGS Sir John Franklin got a new lease on life after universities around Canada decided to pool the money together, and retrofit the icebreaker to use it as a research vessel. It was to be operated by Canadian Coast Guard half the time - so in reality the icebreaker is shared by scientists and Canadian Coast Guard - kind of like how roommates buy a flat screen TV together so everyone can enjoy it at scheduled times. This was the moment when the name was changed to CCGS Amundsen (in honor of Arctic explorer Roald Amundsen).

Interesting facts and information:

- CCGS stands for “Canadian Coast Guard Ship”.

- Roald Engelbregt Gravning Amundsen (after whom the icebreaker is named) discovered South Pole in 1911 and was the first one to reach North Pole in 1926. He disappeared during a rescue mission in 1928 and his body has never been found.

- CCGS Amundsen is powered by 6 diesel engines - 18,000 horse power combined! That is roughly equal to 130 Honda Civics.

- The ship has enough room for 80 people (40 being the crew) and a small helicopter

- She can crash 1 meter thick ice and travel up to 15,000 nautical miles

Canadian Banknotes

Happy Friday! And a little bit of First World Problems

First World problems

I was sitting at my desk and swearing (quietly) at my iPhone for taking forever to update to iOS 7. My phone isn’t the newest - I bought it used for cheap - so it certainly was taking its sweet time. Clearly, it was a pretty bad case of firstworldproblemitis.

First World Problem, noun

Problems from living in a wealthy, industrialized nation that third worlders would probably roll their eyes at.

Example: My 7 dollar starbucks latte came with ONE espresso shot instead of the TWO I asked for!

We all run into small problems that irritate us to no end - but it’s important to put things into perspective. Anyone who lives in North America and is relatively healthy should be dancing in the streets - we live long lives surrounded by wealth and can change our destiny with relative easy by going to school. Most people in the world would be happy to have our everyday problems. Canada is ranked very highly in terms of income mobility. And we have universal health care to boot.

Enjoy your weekend and enjoy life in general!

Best personal finance software - my personal experience and what you should consider

Why do you need personal finance software?

There comes a time in every person’s life when he/she asks a simple question:

” - I work day in and day out. I volunteer for overtime when it’s available. Sometimes I leave for work when it’s dark, and come home when it’s even darker. My paycheck is actually quite decent. When I’m at the store I go for a generic brand of corn flakes as opposed to fancy Kellogg’s just so I can save $0.49 and yet I have way too much month left at the end of the money. Where do my money go and how can I wrangle them back?”

I know it happened to me. I just couldn’t quite figure it out - money comes in, and even though I don’t spend much on anything, it’s always quickly gone. Some people call it paycheck to paycheck living. So, following the advice I picked up in multiple books, I’ve decided to track down my own money (sounds like an adventurous movie!).

The usual approach is to purchase a computer program and upload transactions from your bank to get a realistic picture of where your money is going. You can also use spreadsheets (that sounds like fun, right?) if you’re good with Microsoft Office products. A good old notepad and a pencil will also do the trick if you are old-fashioned.

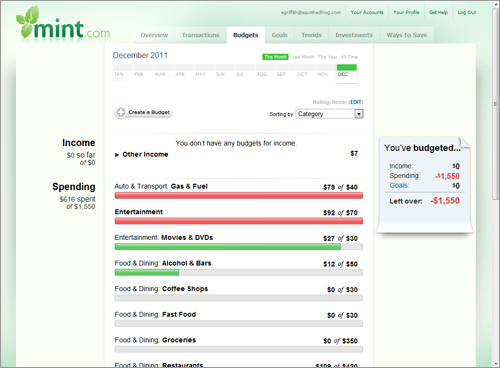

For a couple of years by now, my wife and I been using Mint.com to keep track of all our expenses and plan our cashflow. Mint.com is an online website that lets you keep track of all your finances, keep an eye on your balances, plan and budget your expenses.

Personally, I think tracking our expenses was one of the best moves we did to improve our finances - we felt like we got a pay raise by simply watching where we spend our money.

What makes Mint the best personal finance software?

- It’s absolutely free

Traditional software packages start around $50 and go up as high as $150. With Mint, you’ll never be asked to pay for anything. It doesn’t matter how many accounts you have, how many people in your family use it, or how many devices you use to access it. It’s free. Zero. Nada.

My understanding is that Mint.com makes money mostly by referring clients to services - credit cards, GIC investments, life insurance, and others. I have no need for such referrals so I simply ignore small banners.

- It’s very easy to use

Expensive software packages do offer an array of features. They’ll drown you in a sea of pie charts and break-even analysis. They’ll create complicated debt-repaying plans, and even project your expenses into the future.

But I prefer simplicity over sophistication. I don’t need to see a 90-day breakdown of my expenses by category or graph representation of how little money I have. Thank you very much, I don’t need pie charts to explain it to me. I simply need to know where my money is going on a monthly basis, make sure I’m not overspending, and send me a quick alert if bank account dips below a set mark. Keep your pie charts, they’re not as yummy as they sound.

Best Personal Finance Software

- It uploads all transactions automatically

You don’t have to upload or record transactions. This part is especially sweet for me because I just wouldn’t be able to keep up with the extra work involved in it. I know some people who use sophisticated programs (MS Money, Quicken, You Need A Budget to name a few), and all of them require you to manually download transactions or create transactions when you purchase things. To quote a recent viral video - Ain’t nobody got time for that!

Mint.com automatically downloads all transactions from all accounts, and even does a decent job of classifying your expenses - like putting Superstore or Save-on purchases into “Groceries” spending categories. Quite often you have to change it, but it literally takes 5 seconds on any given day.

- You can use it anywhere

When it comes to traditional personal finance software, you usually install it on your computer. In order to use it, you have to run it from that specific computer unless you buy a mobile application to sync your data. Also, if you’re need to install it on another computer - say you bought a new one or your wife would like to use it too - you’ll have buy additional licenses. Mint on the other hand can be open on any computer using a simple browser. Even if you are in Australia, you can quickly check it while sitting at Internet cafe.

- Fantastic features

Best personal finance software

Mint has a lot of built in features that I wouldn’t be able to live without - it allows you to create and stick to a budget, reminders for bill payments such as credit cards, and sends you email alerts if you’re overspending in any category or your bank account is below your set minimum.

Monthly budgets are very easy to set up especially if you spend some time and do it properly from the very beginning. Once you organized it the way you like it, setting up monthly expenses is a piece of cake and takes about five minutes every month.

Unlike other personal finance software products, Mint allows you to customize your budget with ease. Its simplicity is what really appeals to me - instead of modifying a gigantic chart of accounts in MS Money, you simply add or delete spending categories on the fly.

- It has a kick-ass mobile application

Best personal finance software

They also have an absolutely fabulous mobile application (or “app” as cool kids say) which comes in handy. We often use it when shopping to makes sure we have enough money in our budget and check account balances in one place (as opposed to visiting 2 or 3 banks online). Just like Mint itself, it’s completely free.

Some concerns about Mint.com:

- Privacy issues

Some people are concerned about privacy when giving away their bank information to an online service. And rightfully so - these days identity theft is a very serious problem. Personally, I have no such concerns. Mint.com is owned by Quicken - one of the largest personal finance software company in the world. If anything funny was going on with Mint, it would compromise millions of dollars they are making - companies like this take your privacy as serious as you or even more serious than you.

- Investments tracker isn’t very sophisticated

Mint also allows you to add investment accounts, but I completely ignore this feature and simply use Mint to control my cash flow on a daily basis. I feel no need to check my investments every day. So, my preference is to leave investment side of our finances completely out. If somebody needs to keep track of their brokerage accounts, there are more sophisticated tools for it.

- Cash is harder to track

If you use cash on daily basis, it might make things a bit more complicated - because in this case you’ll have to manually enter cash transactions into Mint. This can be rather painful for some people (including yours truly). Thankfully, me and my wife never use cash and switched completely to debit cards (and one measly credit card) and electronic payments between banks. This way Mint always captures all of our transactions, and lowers the amount of work we need to do to a minimum.

Conclusion (short and sweet):

Mint offers is a fantastic free tool to control your spending and watch your cash flow without paying for an expensive software package. You can use it anywhere you go - on your mobile (Apple or Android), on your home computer, or even your friend’s computer if you’re away (be sure to logout after you’re done). It will make budgeting and financial goal setting completely painless. If you like simplicity, you will like it. All of it makes Mint the best personal finance software in my opinion. Did I mention it’s free?

Pros: Absolutely free, lots of features, easy to use, completely automatic, and platform-independent

Cons: Lacks sophistication with investment accounts, doesn’t have tax component, and sends you occasional marketing pitches for financial products

Action step:

Mint.com has a demonstration website you can visit before you sign up. It has made-up bank accounts and transactions to give you a feel for features and usability. Give it a whirl, check it out! Once you see how useful it is, just sign up and start using it. You won’t look back!

What do you use to keep track of your finances? Please comment and let me know your experience!

The Tale of Two Christmases - Saving for Christmas Presents

Are you saving for Christmas presents? It’s only six paychecks away!

Saving for Christmas presents

Just few days ago, I was out for a walk at the mall. Yes, I’m one of those people who sometimes pointlessly walks around the mall for no good reason - I’m not there to buy anything, I was basically trying to kill an hour or two. I do like to check out certain stores from time to time without actually buying anything - Chapters for books, Apple store for iMacs, electronic stores for all the gizmos, and couple others. You never know when you discover a good book - and new iMac’s are shiny and pretty!

So, when I was walking through Sears, I couldn’t help but notice an open door into their warehouse - and what I’ve seen shocked me a bit. Their warehouse already had Christmas stuff piled up! After initial shock, I exchanged a few words with a clerk (after he made sure I’m fine since I was a bit pale), and he mentioned that Christmas stuff starts arriving just about now.

And that made me think about how we used to buy presents…

Buying presents at our house 3 years ago:

Saving for Christmas presents

Three years ago, we did what most people do around Christmas - get stressed out about buying presents, spending too much money, and then paying off our credit cards well into February. My wife loves giving presents and is absolutely fantastic at finding something special for everybody. I on the the other hand wouldn’t voluntarily step into a mall around Christmas even if they were giving out free iMacs.

Typically, we would wait till December to even start thinking of presents, and that would translate into an obvious money problem - we wouldn’t have much left after all the expenses. Because of that, we’d be forced to put everything on credit cards which would guarantee no sleep for me until they are paid off - and it would cost us since it would be impossible to pay them off in one month. All of this would turn a pleasant process of buying presents into nerve wrecking mall trips and money-related bickering between me and my wife. Absolutely appalling, if you ask me.

Not to sound cliche, but there has to be a better way! And we found it.

Buying presents at our house NOW:

Saving for Christmas Presents

Step one: Make a rough list of all occasions throughout the year.

That includes birthday presents, Christmas presents, occasional visit presents, etc. for ourselves, my mom, my brother’s family, my wife’s family and a few of our friends.

Step two: Get a rough estimate on how much money this represents in total.

Some are small inexpensive presents, while birthday presents are usually a bit more expensive. Keep in mind any weddings coming up or special occasions. Leave some room for error too - add 20%.

(did you know an average American spends $646 on holiday gifts? Seems high to me!)

Step three: Open up a separate savings account linked to our debit card.

Every month transfer 1/12 of the figure from step 2 into this account automatically. This year it came to $130. Your figure might lower or higher - depends on number of people in your family and your standards which are always individual.

Step four: Enjoy stress-free saving for Christmas presents (and other occasions).

Buy presents with money in your savings account when the need arises.

Step five: Re-evaluate every year.

Sometimes the monthly transfer number needs to go up or down. I believe we started with $100, but brought it up to $130 last year.

What a big difference a little planning makes!

Now we’re never stressed out about buying presents because we always have access to money specifically saved for presents. Now my wife can freely buy presents when she sees a good one for somebody. It actually saves us money now since now she doesn’t wait till Christmas season to buy them - and can buy something that is on special at fraction of a price.

At the same time, the financial nerd in me is finally at peace - no longer I’m stressing out about spending large amount of money in short period of time and dealing with debt afterwards. No longer we’re paying interest on credit card purchases. No longer we’re bickering about gift buying during what supposed to be a family time. Life is good!

I strongly recommend this approach of saving for Christmas presents

Not only it will bring you fiscal peace around Christmas, but it will make your relationship stronger by avoiding unnecessary stress. Number one reason why couples fight in North America is fighting over money. One less reason to fight equals stronger marriage.

Think about it - if all the stores are preparing for Christmas well in advance, shouldn’t you preparing too? Good planning always makes life easier for everybody.

Now that Christmas is only six paychecks away, how about a little test drive? Instead of waiting till Christmas to worry about buying presents, how about saving for Christmas presents ahead of time this year? Figure out what you will be spending, divide this number by six, and put the money away - I promise you’ll feel more relaxed when the time comes! You can always go back to unstructured chaos of spending if you don’t like it!

- But what about buying presents for each other?

This is one of the drawbacks of this system - your spouse would be able to see what you buy him/her as a gift. We solved it rather simply - we basically tell each other when we’re buying presents for each other and promise not to look at online statements for a bit. Problem solved!

Can An Average Person Become a Millionaire?

Lottery is the only way to become a millionaire for an average person!

Become a Millionaire

This is the message being repeated over and over in today’s media - rich people are getting richer, and poor people are getting poorer. If you’re not born wearing a top hat and a monocle, your destiny in life is to be poor, and to work till you drop dead. Lottery and inheritance are the only legit ways for an average person to become wealthy and retire with dignity. The only way around is to get lucky and get yourself a union job with pension unless you can invent Google or Facebook. You won’t become a millionaire unless you start your own business.

Rubbish. Poppycock. Nonsense.

Your chances of winning a lottery are virtually non-existent. Inventing Facebook is kinda hard because it’s already up and running. Union jobs are scarce these days, and they are slowly going away, unfortunately. Inheriting money does happen - but do you really want to wait for it? Not to sound morbid, but do you really want to live your life waiting till your well-to-do uncle decides to expire? Besides, it still requires a well-to-do uncle with no kids - and he has to like you!

I must say, I’m amazed at the amount of this misinformation flying every which way in our society. We hear it from newspapers and magazines. In turn, we tell it to our kids and chat with neighbors about it. In our minds, there are two worlds - world of poverty and average everyday struggle, and a magical world of wealth. And nobody can cross the bridge unless they get “lucky”…

Let’s take an average Canadian

Here we have an average 20 year old young male, let’s call him Arthur. He may or may not have a degree. May be decided to take a couple of years off after high school to find himself - whatever that means. Arthur works at Starbucks serving your everyday morning fix - large caffee latte with a yummy blueberry muffin (can’t you tell I’m hungry?). Not exactly a high paying glamorous position, but Arthur is a down to Earth guy and isn’t high maintenance. No rich uncles, no union jobs for Arthur, and definitely no prospects of starting another Google. Can our average guy Arthur become a millionaire?

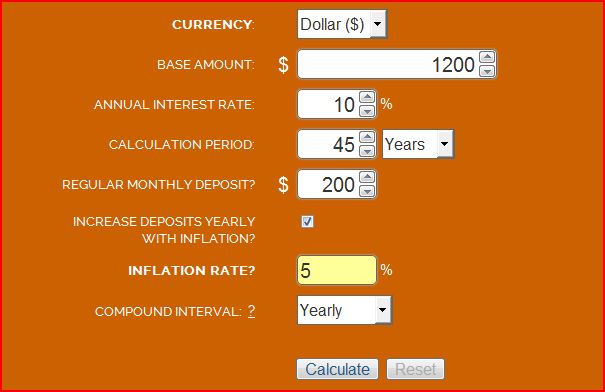

Let’s say Arthur decides to save $100 a month - nothing huge. What’s a hundred bucks to Arthur? Not a big amount of money, average young adult pays a little bit more in cell phone fees these days. Arthur takes $100 every month (or $50 every time he gets paid), and puts it into mutual funds. He’s not a financial nerd by any stretch of imagination, he simply buys them every month without changing his lifestyle or making big sacrifices. And he keeps doing it so for 45 years - through out his adult working life.

He loses his job at Starbucks for dropping muffins on the floor, and starts working at Home Depot - but every month he habitually puts $100 into mutual funds. Arthur goes back to school, picks up a trade and becomes a plumber - yet still every month puts away that hundred bucks into his investments. He even moves out, and meets a very special girl named Cindy and they settle down, have babies, move a few times, have a few fights but make up, go on vacations, fill up a few albums with photos, and finally turn 65.

How much money does Arthur have in his investment account?

By the end of his working life, Arthur is just a bit shy of being a millionaire - he has $996,202.87 sitting in his account to take care of his retirement expenses. Arthur, the average kid with no special skills and very questionable skills of handling muffins, no rich parents, no lottery winnings or Google fortunes, retires as a millionaire and lives happily ever after with Cindy occasionally visiting his kids. The only thing Arthur had going for him was time - and time turned his monthly $100 into a million bucks.

Become a Millionaire

What if Arthur did few things differently?

- If Arthur waited till he turns 30 to start saving money, he would only have $376,312.27. While it’s nothing to sneeze at, it certainly shows that time works to your advantage - and more time you have, the better results will be. Lesson here - start early. Preferably in your teen years.

- If instead of saving $100, Arthur decides to save $200 (or teams up with Cindy by contributing $100/month each for the future of their family), his investment account would hit cool $1,904,937.16.

- If Arthur decides to inflate his savings goal by 5% each year ($200/month first year, $210/month next year, $220.50/month year after that, etc.), Arthur and Cindy would retire as multi millionaires with $3,318,753.74 sitting in mutual funds. I think they’ll be just fine.

Play around with this calculator and plug few numbers for yourself. See what can be done over time with just small monthly contribution. For the sake of argument, I picked 10% as market return throughout - which is very realistic - and $1200 as starting capital.

Become a Millionaire

An average person can become a millionaire

In my mind, there’s just no excuse for anybody born in Canada NOT to retire as a millionaire. And I’m pretty sure everybody knows that saving over time can turn money into more money, but not everybody understands how drastically time can help you. You don’t have to be a financial nerd to become a millionaire - picking mutual funds is as easy as checking your engine oil. You don’t need to make huge sacrifices and eat cat food trying to save every penny - a hundred dollars every month will do. What’s $100/month to you?

The main point of my rant

Next time you hear somebody going off about how average people can’t get ahead, think of Arthur. How an average young adult with some determination can become a millionaire - just by sacrificing few dollars a day to save that $100 at the end of the month. If Arthur with just $100 can do it, so can anybody. No need for lotteries or rich uncles.

Ten Facts About Money (and life in general) I Wish I Knew When I Was Younger

Sometimes I wish I could travel back in time and tell the younger me ten facts about money. I’d probably also tell myself to buy Microsoft, Apple, and Warren Buffet stocks. But I could never find a flux capacitor for my Jetta, so instead I wrote them down hoping it will help somebody else.

Ten Facts About Money

1. You have to pay attention to your money. Otherwise your money will leave you.

Unless your cupboard contains stacks of dollar bills instead of food (in other words if you’re not stupidly rich), you need to know where your money is coming from and how much you’re spending. Simply checking your bank account to see if you have enough money before you buy a sandwich doesn’t keep you informed. You need to control your money, or the lack of it will control you for the rest of your life.

I once talked to a fella who paid double rent for a number of years due to mistake his property management company did. He never noticed it because he never bothered to check his account statements. While he enjoyed a very decent income, he never knew how much money he is spending. Only after running into financial issues the mistake became obvious, but he could have wasted a lot of money until he discovered it himself (if ever).

2. Almost everybody wants to take your money away from you

At the present time, advertising is everywhere. While we might be used to it on Internet or radio, marketing companies are coming up with more and more ways to sell us more stuff. Video game makers now sell advertising space in video games. Your local pizza shop puts advertising for local real estate companies on pizza boxes in case you are so hungry that you want to buy a house. After consuming few beers at your local bar, you head for the washroom and end up staring at beer ads on the wall. Oh, the irony…

There’s a war for your wallet going on 24/7. Be aware of it, pay attention to sleek marketing schemes, and don’t fall for advertising. Your personal and family needs should be dictating your spending habits, not advertising.

3. Wealth is not evil

Books and movies teach you stereotypical knowledge about money. Rich people are not all jerks, and poor people are not all gold-hearted. Portraying them this way helps to sell more books and movies, but it’s far away from reality. Money doesn’t turn anybody into jerks. Money just intensifies people’s desires. If somebody has a heart of gold, they’ll spend money helping people around them - not matter how much or how little they have.

Think of money as bricks. If you have a lot of bricks, you can build a hospital for everyone’s benefit. Or you can build a wall around your house to keep people away. It’s what you do with bricks that counts, not the fact that you have a lot of them.

4. Looks can be deceiving

Just because somebody has a shiny new car doesn’t mean they’re rich. Just because somebody rides a bicycle to work doesn’t mean they’re poor. Don’t judge book by its cover, and don’t judge people by their appearance. You’ll be surprised how many seemingly well-to-do people bounce credit cards, and how many seemingly blue-collar folks can live without income on their savings for years if they were to lose their jobs.

5. Forget about getting rich quick

If there was a legit way to get rich quickly, everybody and their uncle would be doing it.

6. Be the best at what you do no matter what you do

Younger me went through a lot of crappy jobs. I washed cars for living, cooked burgers, delivered Yellow Pages, and cleaned houses. Not exactly dream jobs - and keeping this in mind, I didn’t try to be anything above average. ” - Why bother?”, I thought. “- When I get that cowboy-astronaut-millionaire job, I’ll be an absolute rockstar! But this job is just for getting by at the moment, no need to show off.”

Now I see how wrong I was. If you work like a lazy sloth (and sloths are pretty lazy since they sleep up to 18 hours a day), nobody will ever offer you that dream job. Be awesome at what you do - even if it’s flipping burgers or waiting tables. The next customer you wait on might end up leaving his business card asking to call him for an exciting position - after you blow him/her away with your people skills. Only the best people get noticed - because they stand out.

7. Rainy day is coming

Ever heard of the infamous “rainy day”? It’s coming. Be prepared for it - have insurance in place, have emergency fund set aside, have wiggle room with your money. While some people might say “You have to stay positive!”, I can positively say the rainy day will come.

8. Spending leads to more spending

There’s nothing wrong with owning nice things! But you have to look at how they affect your money beyond just one purchase. Big houses usually come with higher property tax bills, higher utilities, and more time wasted on cleaning it (or money spent on cleaners). Luxury cars feel great, but most require premium gas (expensive!) and higher insurance premiums (expensive!). Your new TV will require gold-plated audio cables - or at least that’s what the sales guy will suggest. Even a cute puppy comes with an array of expenses - not matter how cute it is.

9. Humans are creatures of habits

Habits will play a huge role in your life. Most of the things you do are very habitual - from food you eat to the way you dress. For example, I’ve had the same thing for breakfast for the last few years - oatmeal with raisins or fresh fruit. I can almost make it blindfolded - but don’t do it fearing my wife will make me clean the kitchen.

While some habits are harmless and won’t affect your life, some habits can be absolutely devastating to your finances or life in general. Habitual smoking or gambling come to mind right away. At the same time, you can pick up some good habits that will benefit you along the way - preparing a monthly budget or making your own morning coffee will make it feel like you’ve got a raise.

10. Be aware of small expenses and fees

Small expenses add up over time. An occasional late payment on your Visa card translates into few hundred dollars paid to the bank over a year. Satellite radio - which you haven’t used since you bought your new car - only costs few dollars a month, but once again adds up to substantial amount of money. ATM fees, morning coffees, iTunes purchases, online games, etc. all cost very little and something along “Oh well, it’s just 99 cents!” passes through your mind when you buy them. But feel free to add them all together and look at how much money is leaving your wallet. Death by a thousand cuts, eh?

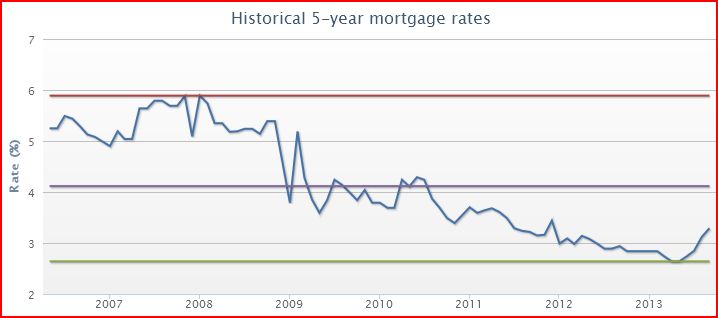

Rising Mortgage Rates in Canada - What happens if the rates double?

Rising mortgage rates in Canada?

Rising mortgage rates in have been discussed for quite some time. As you may or may not know, mortgage rates in Canada are tied to Bank of Canada lending rate - banks borrow their money from Bank of Canada, and then turn around and lend money to you and me. Of course, they charge a bit extra - after all, they’re in business of making money, not simply passing it around. Once you understand this, it’s easy to understand that Bank of Canada lending rate is tied to mortgage rates in general. If Bank of Canada brings their rate up, almost all banks follow the trend and raise their rates - because they don’t want to lose money. Three days ago, Bank of Canada made an announcement that interest rates will be staying where they’re now for now.

Rising Mortgage Rates in Canada

But it’s important to understand that currently mortgage rates (and other lending rates) are at historical lows. If you ever talk to old-timers, they’ll remember the rates being in double digits - 15-20%. Rates have been falling over the years - and with last recession Bank of Canada cut them to never-seen-before levels. Where will they go from here? I think it’s safe to say that they have nowhere to go but up. The economy is coming around, and sooner or later our government will have to do something to prevent it from running away again - and interest rates is one of the ways control it.

What are you paying now in interest?

If you ask somebody about their mortgage rates, they’ll probably respond “Oh, I’m paying around 3% currently”. People who pay a bit more attention to their finances will say “My monthly mortgage payment is $1200”. Somebody who is borderline obsessed with personal finance (that would be me) will say “My by-weekly mortgage payment is $495.17, and I pay my bank 3.89%!”.

Your mortgage payment consists of two parts - principal repayment (amount that goes towards paying off the house) and interest payment (amount the bank gets for lending you money). Lumped together is the amount leaving your bank account every month (or by-weekly if you’re on by-weekly payments). If you ever want to get depressed quickly, ask your bank how much of that amount is interest and how much goes towards the principal. Just because I had nothing to do, I called my bank:

$157.99 Principal Payment + $337.17 Interest Payment = $498.16 Mortgage Payment (by-weekly)

Good god, somebody give me some wine. My mortgage payment is mostly interest charges! No wonder banks have such nice buildings.

What happens if the mortgage rates double?

Currently we’re paying 3.89% on our mortgage - which was a good rate when we bought our little home, not so good right now. Historical average for mortgage rates over the last 30-40 years is actually closer to 8 percent, or roughly double what it is right now for us personally. In two years, we’ll have to refinance our mortgage since our 5-year term will be up - but what kind of rate will we get? And with all the talk about rising mortgage rates in Canada - I got curious and decided to do some math.

Quick and dirty math on our mortgage payment if our rates double. The real number would be slightly off - because by that time our mortgage amount would be lower but that’s why I call it quick and dirty:

$157.99 Principal Payment + $674.34 Interest Payment = $832.33 Mortgage Payment (by-weekly)

Good god, I need more wine. If the interest rates indeed double in two years, our mortgage payment will be over $800 (by-weekly) - which means we’ll be paying over $1600/month.

Can we afford it? Well, it will certainly put a break on our saving rates - currently we’re saving quite a bit for the future as many financial advisors recommend. If the mortgage rates double (and I doubt our income will do the same thing unless I start removing my clothes for money), most of the increase will have to come from the money we’re currently saving. The result? Less money being saved for the future, less money for consumption, and a whole lot of wine being bought.

How will rising mortgage rates affect you personally?

Ask yourself few questions - what is your current mortgage rate? How much are you paying in interest and principal payments? What happens if mortgage rates return to their historical average, will you be able to afford your house? Will you have to adjust your life?

While many people might be scared of rising mortgage rates in Canada, one thing you can do to punch fear in the face is to educate yourself. At least once you know your situation and facts, you can make an educated decision to worry about them - or not.

Once you educate yourself, you can look at some options - refinancing your mortgage to lock into current rates or even extending your mortgage term to 10 years. You can also increase your current principal payment and accelerate your mortgage repayment - this way your principal amount is lower when you’re refinancing.

Resisting The Urge To Buy - My Way Of Saying “NO!” To Myself

Resisting The Urge To Buy

Saying no to yourself can be hard. We’ve all been there - here’s this new thing we have in our mind. It’s shiny, new, and it’s absolutely awesome. It has all the latest bells and whistles. It’s high definition and it grills better burgers. It has better gas mileage and better upholstery. And it’s on sale! Whatever that is - I want it. Good god, I want it now, and I deserve it!

But I also know I can’t go around buying stuff. Between paying for everyday expenses such as mortgage, groceries, gas and bills, saving for larger purchases, and investing for the future, money tends to run out fairly quickly. If I acted on every single urge that comes in, I’d be out of money (unless I bought a money tree, but I haven’t seen one for sale).

Why is it so hard for me sometimes?

What makes things especially hard for me is that I get excited about new things very easily. My mind quickly jumps into rationalization mode and shows me 17 ways this new thing will make life awesome for me. If it’s a new barbecue, I can almost smell the freshly grilled meat and hear the noise of a party in the background. If it’s a car, the brain paints me the picture of long road trips in a shiny new car. If it’s a gadget - all the ways this new gadget will make me more productive.

People (and myself especially) are masters of rationalization. We can turn a “want” into “need” with a lightning speed. My mind almost whispers into my ear how I deserve this new thing - and why I should have it. ” - Come on, you’ve been working hard. It’s time to treat yourself a bit. You deserve it!”.

Grills quickly become investments into relaxation that we so badly need. New SUV - investment into safety (even though SUVs tend to be less safe to begin with). New iPhone - an investment into productivity (although the other iPhone was just as fine when it comes to Angry Birds).

My “magic” system to resisting the urge to buy!

Over the years, I’ve figured out the ways to drastically cut down on impulse buying - especially when it comes to larger purchases.

- Step 1: Think back to all the things I wanted to buy … and didn’t.

By now, I have a list of things I really wanted to buy but didn’t. Some of them look silly by now, some are quite reasonable but timing was wrong. Every time I get the urge to buy something, I look back to my experience, and think “Will it be like this time I wanted to buy … and didn’t? Will it look silly after a while as well?”

Chevrolet Camaro IROC-Z

Resisting The Urge to Buy

For some reason, I really wanted to buy this car when I was much younger. I even looked at few for sale, but after a while my interest in it fizzled away. And thank goodness - the thing is butt ugly.

Honda Silverwing motorcycle

Resisting The Urge to Buy

Just like anybody else, I went through “I want to ride a motorcycle” phase. I even saved up some money, and started looking around for used ones to buy. After a while, I found a decent Honda for sale, and met with the owner. The bike was in great shape, but I can’t say the same thing about the owner - he was using crutches. Apparently, he had a small accident on a motorcycle just few weeks ago that left him with broken legs, and that was the main reason for selling it. Let’s just say I lost interest in riding bikes on the spot.

Compaq iPaq handheld computer

Resisting The Urge to Buy

This was a hard one. The technology nerd in me was going overdrive screaming I really really need this. All the features appealed to me. I imagined myself being super productive with it, scheduling events, and sending emails. After waiting for few weeks, I’ve discovered the fact I can send emails just as easily from my computer, and scheduling works just as fine with a small notebook if needed. I wonder if these things are still around? Looks rather archaic by now.

- Step 2: Save money in cash

I made a promise to myself to never ever buy anything on credit. Every single purchase I make is only done with cash - and cash is saved up no matter how long it takes. Sometimes it’s just couple of months, sometimes it takes much longer - but I always save money in cash. Credit sure makes purchases easier - these days you can even buy pets on credit - but credit also makes it easier to follow through on foolish decisions.

- Step 3: Think how this purchase fits into my plan

Ultimately, you always want to be somewhat utilitarian. Ask yourself - what benefit will you get from this new purchase? How will it benefit your life as a whole? If you have goals you’re working on - how this new purchase helps you achieve them? Some purchases truly benefit you and your family - a second car will allow your partner to bring in a second income or make your life easier. A new flat screen TV (slightly bigger than your other flat screen TV) on the other hand doesn’t carry any benefits because the other TV is just as good - just smaller. Is high definition really worth the money?

- Step 4: Revisit the idea once money is saved up

Once I have the money in hand, and I’m staring at the item I want, I revisit the idea of buying it one more time. Do I still want it? Does it still appeal to me? I’ve worked really hard to save up the money and can almost see the sweat dripping from it - do I really want this new thing?

Countless times, I’ve walked away from the deal at this point of buying. For various reasons, I just didn’t want to go through the process after all the time and effort I put into saving the money.

Short version - just be patient.

Whatever your system to resisting the urge to buy, it all comes down to patience. Each of us has a couple personalities inside of us - rational frugal personality and “Oh good god, I want it now!” personality. One wants to follow the plan, stick to a budget, and save money. The other one is looking for party and good times. The party personality wants to buy the world, the frugal personality wants to save money and do boring things with them (such as investments, saving for the future, etc.). The best way to fight the urge to buy is to insert time between the urge and actual buying - chances are by that time my party personality moves on to wanting something else. Saving money in cash allows the time to pass and some common sense to kick in.

Hope this helps you with resisting the urge to buy!