It’s been a while since we’ve talked. Five years ago I’ve walked out on you. Five years ago I’ve decided to end it with you. And these five awesome years were filled with joy and happiness. In all honesty, I don’t miss you one bit.

We’ve met when I started going to college. A sweetheart counselor thought she’s doing me a favor by introducing me to you. See, I was new to this country, and didn’t know anybody, so it felt nice to have somebody to rely on. Too bad I’ve never finished college and had to go back to work, but you’ve stuck with me even after I dropped out.

Heck, we had some good times together

My life felt easier when you were right next to me. You took me places, you bought me stuff. I remember going on a trip to Europe with you, and you made it extra sweet for me. You paid for hotel, my meals, and even an awesome camera I just had to have before heading there. I still have pictures, dear Debt.

I remember you buying me a new car. You felt I deserve something better to drive because my old car was not as shiny as new ones, and didn’t have fancy options. At first, I resisted but you’ve talked me into it by saying how hard I work and I deserve to enjoy finer things in life. So, you bought me a new set of wheels, and after parking my old car in a garage (hurt feelings!) I started driving in style, just like all of my friends.

All good things end

What started as a fun flirt on a side soon turned into a nightmare of a relationship. Before I knew it, you basically moved in with me. Good memories of trips together were long gone, but you were right next to me every day. Every night you kept me awake as I crunched the numbers in my head trying to figure out how I can make it work. You forced me to work on weekends to bring more money home to pay for you. All of my money was going towards you, but you kept demanding more and more. Your collecting friends started calling me at night asking about money. You made my food taste bland and every day seemed joyless because you sucked the life out of me. You have no idea how bad you make people feel. Heck, some people commit suicide because you got a hold of them.

This is when I said I’ve had enough.

Breaking up with you was hard but truly worth it, dear Debt. I’ve kicked you out of my house, sold your presents, and got rid of your shiny new car. Took me months to clean up your mess! But my old car was happy to see me, and in all honesty I don’t miss any of your presents. I sleep well at night, and my new friends Budget, Savings, and Investing take good care of me. We spend a lot of time together, and I haven’t thought of you for a while now. Because of them, things are looking up for me! All because I’ve made a decision to end it with you.

Dear Debt

I’m glad you’re gone, dear Debt. Don’t ever come back. Forget my number, and forget my house. You’re dead to me.

Lately, mortgage investment corporations have been getting an increasing amount of media attention. Yet if you’re interested in investing in general, there’s very little information out there on what mortgage investment corporation (MIC) is and how one can benefit from them. I’ll try to explain it to the best of my abilities and even share my personal experience with one.

MICs are investment vehicles that focus primarily on mortgages. Thousands of investors pool their money together. Then a newly formed MIC starts lending out the funds to qualified borrowers. MICs are professionally managed by a management team that is compensated with management fees and incentified with a partial cut into profits.

Mortgage Investment Corporation

In reality, mortgage investment corporations are just like banks. Banks borrow money from depositors and lend money out to borrowers. The difference between the amounts of money they make from lending and interest they pay to depositors is their profit.

Somewhat similarly, mortgage investment corporations raise their capital from investors, lend the money out, and funnel the profits back to investors. Some of them choose to also borrow money from banks at low interest rates - but not all of them.

There are many MICs currently on the market, some private and some public. The amount of money flowing into them from investors attracted by very reasonable yield is always exceeding previous years numbers. Largest players in this market include Firm Capital, MCAN Mortgage Corp., Timbercreek Senior MIC and Trez Capital MIC.

While the amount of capital under management and lending guidelines vary from company to company, the general business model behind generating income is very similar between them.

Why I’ve decided to invest my money into MIC:

I’ve stumbled into MICs almost by accident. At the moment, I wanted to park some of our money in a investment with good returns, but at the same time somewhat liquid - meaning we’d be able to get the money out even if it meant paying a penalty.

High interest saving accounts offered by major banks do not offer meaningful returns these days - you’ll be lucky to get anything over 2%. On the other hand, putting money into an index or mutual fund (even with stable history of returns) didn’t seem appropriate for this money. Hey, I like mutual and index funds just like any other guy, but we all know they can go up and down rather wildly.

Investment

Through our financial advisor, we’ve found Crossroads DMD - a Calgary based mortgage investment corporation. They’ve been in business for a number of years, and pride themselves on delivering outstanding returns to their investors while operating a portfolio of many millions under management. This includes first and second mortgages, bridge financing, and construction loans.

Unlike conventional mortgages, these types of mortgages come with higher interest rates. While some people might say it’s because the risk is greater (and honestly, I tend to agree with them to some degree), one must understand this area of financing is very under-served and thus the amount of capital available is limited. Big banks that come with big capital prefer to deal with conventional mortgages, so smaller companies like Crossroads DMD are able to capitalize on small and medium-sized loans in this specialty market and command higher interest rates because of it.

When they lend out investors money, borrowers put their properties on the line. This means these mortgages are secured by real hard assets thus minimizing the risk to investors. They won’t lend out more than 85% of the asset value - which means even if the borrower goes belly up, the investment corporation will be able to recover the funds.

Over the last several years, Crossroads DMD delivered on average over 10% to their investors in form of dividends. Since inception, the average rate of return is 10.6% per annum.

This particular investment also features hurdle rate - a specific target for return on investment that must be reached before the profits are distributed to shareholders. Investors get paid first! Investors also get a 10% share of the profits above the hurdle rate thus benefiting from great performance of the management team. What a great incentive for the management to deliver good returns.

While the investment is liquid and money can be returned to you upon request, an early exit fee (sometimes called “retraction fee”) will apply if money is withdrawn before 3 year mark.

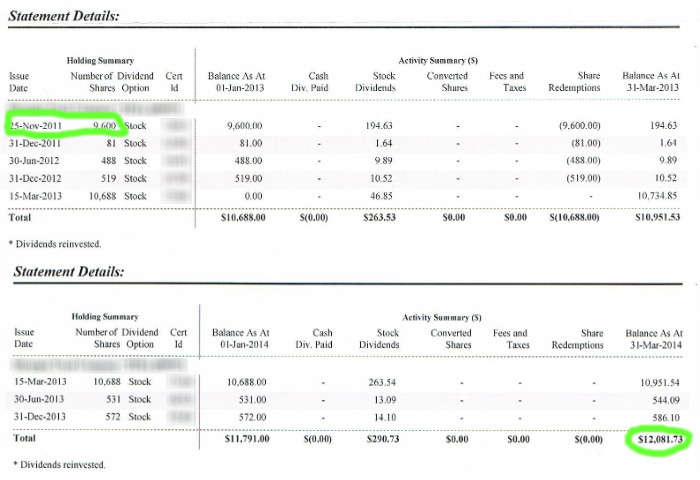

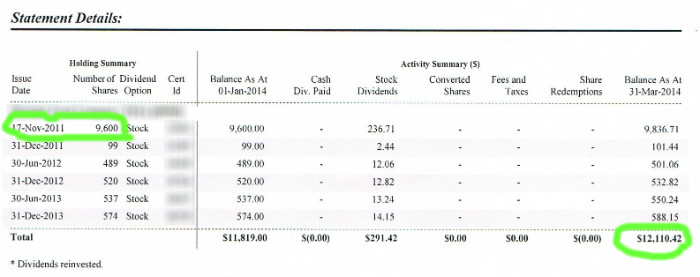

Here’s a snapshot of our investment:

Amount invested (Nov. 17, 2011): $19,200 split between two TFSA accounts.

Investment balance (Mar. 31, 2014): 24,192.15

Mortgage Investment Corporation

Mortgage Investment Corporation

Return on investment: 10.44%

Personally, I’m quite happy with this investment. While some index funds showed outstanding gains over the same period of time, I feel like this is a more stable investment for me. The returns are stable even through tough times! The management team does a great job taking care of investors’ money, and the dividends keep dripping steadily into account. Also, while I might have to pay an exit fee, I have the access to these funds at any time.

All in all, good place to park the money for 3 to 5 years with fairly predictable outcome.

Mortgage Investment Corporation is not for you if:

- You are not comfortable with taking risk

Let’s be honest, the great market crash of 2007 is still not that far behind us. Lots and lots of real estate investments went belly up or taken a serious hit, so some people might not be comfortable with the idea of investing into a mortgage company. I know my first reaction was like that! But after reviewing company’s strict lending rules and their historical returns on investors’ money, it became clear to me that the management in charge of investors’ money is absolutely top notch.

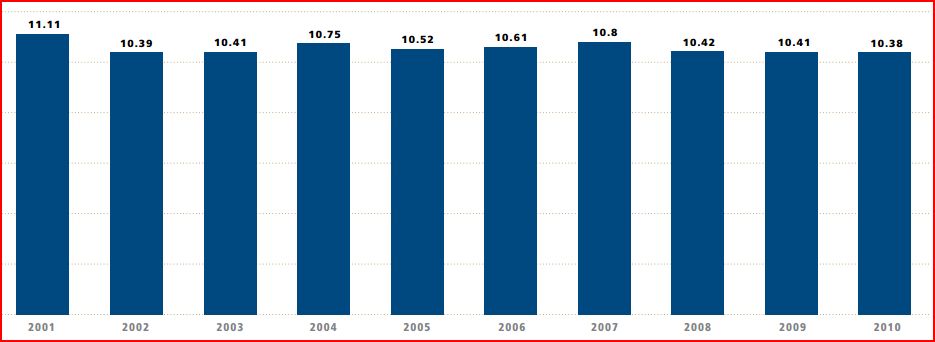

Here’s a snapshot of returns investors received over 10 years:

Mortgage Investment Corporation

Notice how returns have not changed much during our last real estate crash? Yes, the returns went down by 0.4% but never dipped below their hurdle rate of 10 percent. This means their lending practices are very conservative, and their performance doesn’t correlate with real estate market performance in general.

But I’m not going to sit here and tell you this investment is completely safe. The risk is always there, and you have to be comfortable with risk. This is not a magic investment that combines higher than average returns and low risk! Mortgage investment corporations can and do go out of business, so approach this type of investing with caution. Do you homework, read the memorandums, and do research on past performance and current management team.

Putting your money into a mortgage investment corporation is not very exciting. There are no stratospheric returns to brag about. Mortgage investment corporations are not widely mentioned on the news like latest Facebook IPO. You simply put your money in, and it starts dripping dividends into your account in a form of cash distribution or reinvestments. You won’t hear from them unless you receive a statement with your earnings. And if you’re trying to impress your friends with this investment at the next cocktail party, most likely you will put them to sleep explaining what they do.

Some investment can be exciting. For example, one of our investments in solar energy is truly exciting to me because of the difference it will make in Ontario. Green! Solar! Energy! Sounds pretty cool, eh? Mortgage investment corporation on the other hand is a very predictable and boring investment that simply drips dividends into your account. Yawn.

Here are some of my dreams and goals (in no particular order) I’m trying to accomplish. Some of them are silly. Some of them are outright insane. Some are just mine, and some me and my wife share together. And some are rather simple.

Incidentally, not all of them have revolve around personal finance or investing although this is the main subject of my little blog. At the same time, if we ever get to financial independence status, achieving them might become a little bit easier.

I’m a big proponent of investing money. While a lot of personal finance books and blogs usually focus mainly on cutting down your expenses and living within your means, I don’t think anybody ever got to financial independence solely by clipping coupons.

No, I’m not saying you should not save money. Saving money is great, but I think it’s just a part of the puzzle. If we ever want to reach financial independence, we need to wisely invest our money so it multiplies many times over. This is why I’ve always thought that part of our income should go towards investing.

This is way we’re putting down $10,000 (holy crap, that’s a lot of money!) as an investment. The documents have been signed and mailed, cheque cleared, and soon we’ll receive share certificates along with our first monthly distribution.

Investing in solar energy?

My investment of choice is Solar Income Fund.

Solar Income Fund (or SIF) plans on acquiring/developing and operating a number of solar energy farms, mostly in Ontario. Some solar farms will be brand new, some will be existing operations. Just like income-producing rental homes, once built solar farms can be bought and sold by companies involved in investing in solar energy.

Investing in Solar Energy

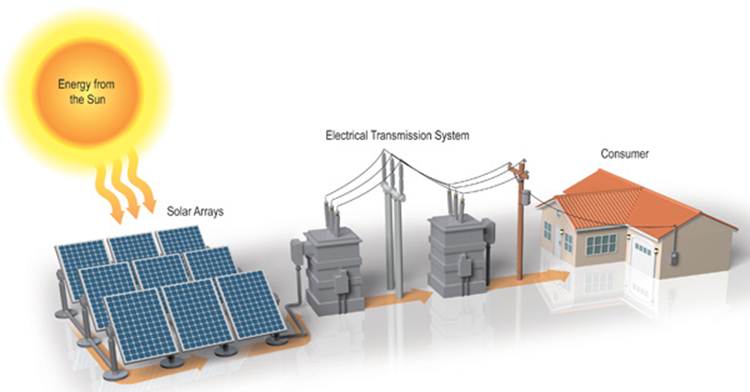

In case you’ve been living under a rock, solar farms are awesome and environmentally friendly way of producing electricity. An array of solar panels is installed on rooftops, farmland, or just open space to convert solar energy into electricity. Electricity then gets transferred into provincial electricity network and the owner of the farm gets paid for the amount of electricity produced. Solar panels don’t need to be maintained and are very self sufficient. They’re even insured against catastrophic events which would stop them from producing electricity and thus income.

Investing in Solar Energy

The Solar Income Fund management team will select solar farms based on their viability, location, power-purchase agreements in place, and long term sustainability.

What makes investing in solar energy in Ontario appealing is the fact that Ontario government guarantees their feed-in rates for 20 years. This means once the purchase rate for a solar farm has been established and the system has been hooked into the system, the price Ontario government will pay for the electricity produced is guaranteed for two decades. Power purchase agreements (PPAs) remove a lot of risk associated with investing in solar energy simply because it makes the investment very predictable.

Why would Ontario government do this? This was part of Green Energy Act that was passed in 2009. Basically, Ontario plans to get away from energy produced by coal to solar energy because solar energy is much cleaner and efficient. They already shut down 19 coal units and remaining coal plants will be shut down by the end of 2014. The energy they have been producing will have to be replaced by solar energy farms. This is where third-party investors such as Solar Income Fund come in and invest their money into solar energy installations and start producing electricity.

Returns and exit strategy

- The investment pays 9% annual return on investment paid out monthly via cheque or direct deposit. This is what’s called “hurdle rate” - until the company pays this out, the management of the company doesn’t get to enjoy the profits. In other words, it is in management team best interests to exceed the 9% rate of return on investment.

- Any income in excess of 9% is split between the investors and the management team with investors getting 60% of the extra income (while management gets 40%). The excess income is distributed annually to investors.

- This is not a liquid investment that you can buy and sell any time you want. Unlike public company stock that can be bought and sold on the open market, this is a locked investment. Once the capital is raised, the fund is closed for further investments and money is put towards purchasing of solar farms. The management plans to sell the fund to an institutional investor (bank, investment company, pension fund, or anyone else looking for a stable income producing investment), and return the capital to investors with an upside profit.

- Income produced with this investment is very tax-efficient. Capital gains are another story though.

Risks and concerns

Just like any investment, Solar Income Fund comes with risks and concerns. After mulling them over, I still went ahead with the investment since I think risks are well managed and thus minimized. But here are a few things that crossed my mind:

- Ability to produce consistent income.

This was my first concern about this investment. Nine percent return seemed high comparing to other dividend paying companies, right? But after looking at some numbers, nine percent looked very attainable. Solar power installations are money making machines! Once they’re built, they don’t require any expensive maintenance. Solar panel manufacturers guarantee their performance. The amount of money solar farm can produce can be predicted in advance given location and technical data.

Once the solar farm has been purchased or built, the money just keeps flowing in. Imagine being an apartment building landlord with extremely predictable tenants. Also, imagine that the government of Ontario guarantees that rent checks will keep getting mailed to you. All of a sudden, the risky business of being a landlord becomes very predictable and profitable.

- Flavor of the month investment?

As soon as I heard “solar energy”, I thought I’m about to hear a lecture on how green this investment is and how awesome it is for the environment. Solar energy has been around for ages by now, and always been a bit of hype. But solar energy in Ontario is there to stay. Ontario government guarantees their solar energy rates for 20 years, so the income that can be produced with solar energy isn’t going anywhere any time soon. Yes, it is a green investment, and will make a huge difference on Ontario’s environmental footprint. I’m super excited to be investing in solar energy because it’s green and pollution-free. But it will also produce income and hefty return for investors in the mean time.

Since 2003, Ontario reduced their coal-fired power use by 90%. By the end of this year, they plan to shut down remaining power plants, and make up for the loss in their energy output with solar farms. Almost 90% of solar farms installed in Canada are located in Ontario. Given all of this, investing in solar energy doesn’t sound like flavor of the month, more like a fundamental change in energy business in Ontario (with rest of Canada to follow, I hope).

By the way, the biggest players in solar energy market in Ontario are TransCanada and Enbridge. I don’t think they’d invest over one billion dollars combined in solar energy if it was just a flavor of the month investment 🙂

Heck, even Dragons Den moguls agree that they missed out on a great opportunity when it comes to investing in solar energy (scroll to 10 minutes 30 seconds mark):

- Experienced management team?

You can have a great business model and awesome prospects for profit, but an inexperienced team can ruin any business and you’ll kiss your money goodbye. After watching enough Dragons’ Den episodes, the role of the management team seems like a paramount factor in business success. This is why you should only invest in companies that have excellent management teams with lots of experience.

It just so happens that these cats have plenty of it. This is not the first solar energy fund they’re starting in Ontario. Including this one, they’ve started five solar energy funds; some of them already exited (have been purchased by an outside investor) with hefty returns touching on 18-19% (not too shabby!). While past performance doesn’t guarantee future results, this still instills confidence in their management team for me. I think my money is in good hands!

What’s next?

Now we’re just looking forward to receiving monthly checks in the mail that will put to use by investing it further into something else. When the fund exits and gets sold to an institutional investor, there should also be an upside return, which will come back to investors along with principal. It might take a while, but it sounds like the money will be hard at work all this time.

Also, next time I’m in Ontario, I really want to visit some of these solar power farms in person just to see my money at work! If this ever happens, I promise to post a picture of me right next to a solar panel! 🙂